TheFinQ.com is designed to be your one-stop destination for everything related to cards, loans, and investment products across India. We help you compare and choose the best financial products that suit your needs, including:

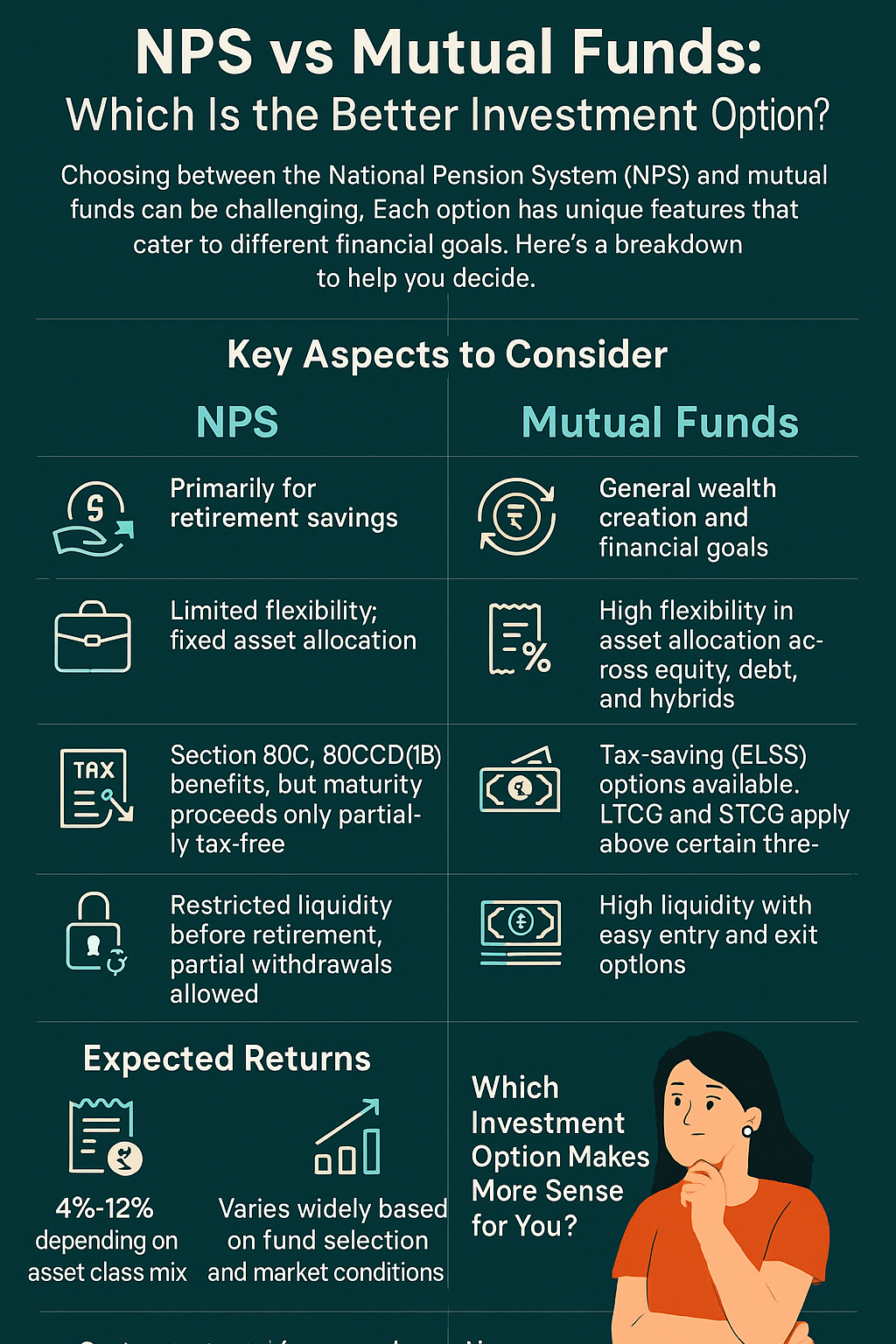

When it comes to saving for the future, especially for retirement or long-term goals, Indian investors often find themselves stuck between two powerful options — NPS (National Pension System) and mutual funds. Both are designed to help you build wealth over time, but they work differently and offer unique advantages.

The big question is — which one can give better returns, and which one suits your personal financial goals?

In this article, we’ll break down both investment options, compare their features, returns, tax benefits, and risks to help you decide where your money can grow smarter.

NPS is a government-backed retirement savings scheme managed by the Pension Fund Regulatory and Development Authority (PFRDA). It is aimed at encouraging individuals to invest regularly for retirement.

When you invest in NPS, your money is managed by professional fund managers and split between:

You can choose how your money is allocated or let the system manage it for you automatically (auto choice).

At retirement (age 60), you can:

Mutual funds are market-linked investments where your money is pooled with other investors and managed by professional fund managers to invest in:

You can choose a mutual fund based on your goals:

Mutual funds offer full liquidity, meaning you can withdraw your money any time (except in locked funds like ELSS).

Let’s compare NPS and mutual funds based on some important parameters:

| Feature | NPS | Mutual Funds |

| Returns | 8%–10% (historically) | 10%–15% (varies by fund type & risk) |

| Tax Benefits | Up to ₹2 lakh under Sec 80C & 80CCD(1B) | ₹1.5 lakh under 80C (only for ELSS) |

| Liquidity | Locked till 60 years (partial after 3 yrs) | Highly liquid (except ELSS – 3-year lock) |

| Maturity Withdrawal | 60% tax-free, 40% annuity (taxable) | Fully flexible and taxable as capital gains |

| Risk Level | Low to moderate (limited equity exposure) | Varies from low (debt) to high (equity) |

| Control & Choice | Limited (especially in auto choice) | High control — choose fund, theme, risk |

| Retirement Focused? | Yes, designed for long-term retirement | Not retirement-specific, but flexible use |

Mutual funds generally offer higher returns over long periods, especially equity mutual funds. Historically, many equity funds have given 12–15% annual returns over 10–15 years.

NPS returns have ranged between 8–10%, depending on asset allocation and fund manager. Equity exposure in NPS is capped at 75%, so even in the best years, NPS may not beat aggressive mutual funds.

Verdict:

For higher returns, mutual funds — especially equity funds — have an edge.

Verdict:

For tax savings, NPS offers greater tax benefits, especially with the extra ₹50,000 under 80CCD(1B).

Verdict:

For flexibility and liquidity, mutual funds outperform NPS.

Verdict:

For low-risk, long-term investors, NPS is safer. But for young investors looking for growth, mutual funds are better.

Verdict:

If your sole goal is retirement with discipline, go for NPS. But if you want flexibility and higher wealth creation, mutual funds (especially SIPs in equity funds) are more rewarding.

The answer depends on your goals, age, risk profile, and discipline.

Why choose one when you can benefit from both?

Start SIP in mutual funds for flexibility and contribute regularly to NPS for disciplined savings.

NPS and mutual funds both have their pros and cons. While NPS ensures security and tax efficiency, mutual funds give you the power of compounding, flexibility, and faster wealth creation. The best strategy is to align your investments with your life goals and risk capacity.

By mixing both, you can enjoy the best of both worlds — stability with growth, and discipline with freedom.